Your Career Is Your Biggest Asset (And That’s Why You Need Financial Freedom)

Most of us work to pay the bills. Some of us even manage to save and invest a portion of what we earn. But few people stop to think about this:

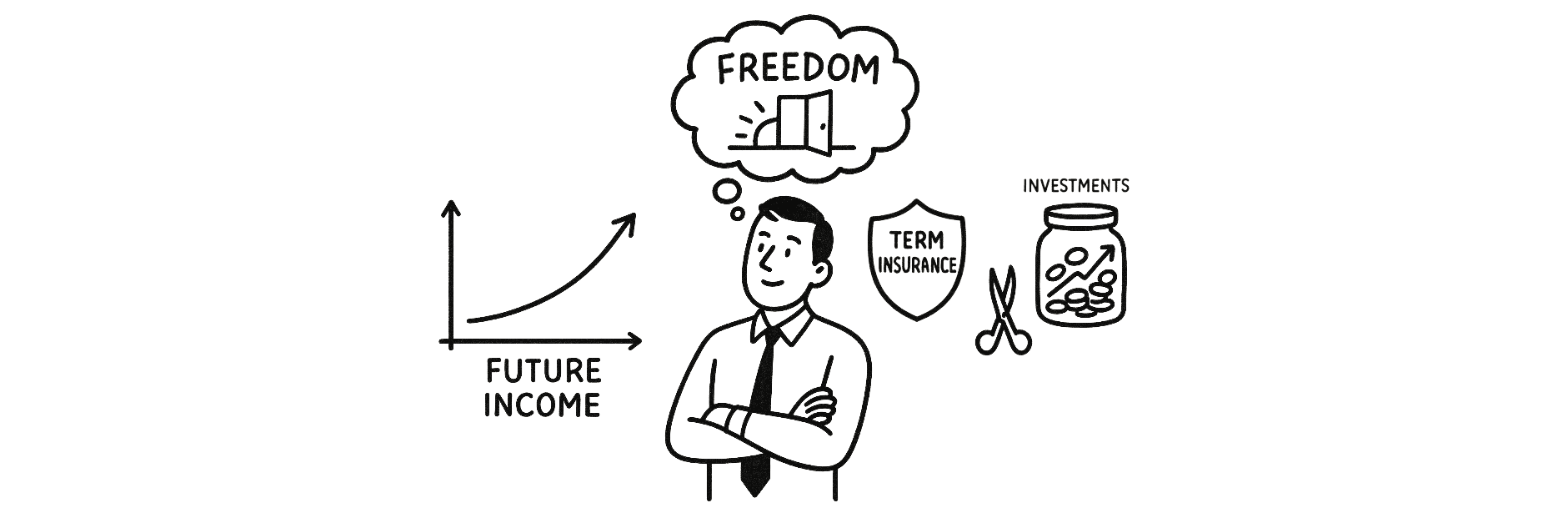

Your career is your biggest financial asset.

If you’re in your 30s or 40s earning $8,000 a month, that’s almost $2 million in future income still ahead of you before retirement. Yet we often put more thought into which stock or ETF to buy than how to manage and protect that income stream.

At RetireBy50.me, we believe financial freedom isn’t just about retiring early. It’s about having the freedom to choose the work you want to do, speak up for what matters, and walk away from what doesn’t align with your values, without fear of financial ruin.

Every week, I’ll be sharing practical tips and invaluable knowledge to guide you on your path to financial independence.

Thinking of Your Life as a Portfolio

In a recent Chills with TFC podcast episode, Alex Lee, a former insurance regulator, ex-CFO, and Chief Actuary shared how he approaches his life.

“The way I look at my finances is I look at my life as a portfolio. For a young person who just started working, your biggest asset isn’t your bank account. It’s the value of your future income.”

He also shared how he intentionally balanced risk in his career with caution in his investments.

Knowing that he had a bold, outspoken personality that could sometimes offend higher-ups, he didn’t try to take on high investment risk on top of that. Instead, he lived simply, built buffers, and adopted a defensive investment approach.

Having financial freedom gave Alex something most people overlook. Psychological safety.

It allowed him to:

- Speak up when something wasn’t right

- Say no to misaligned projects

- Raise concerns even when it ruffled feathers

Financial Freedom = Freedom of Speech (and Self)

Most people think of financial freedom as a dollar figure. A magic number where you can walk away from work forever.

But for many mid-career professionals, financial freedom is about something far more powerful.

It is the freedom to be honest (in my case, brutally honest) in your work.

It’s the ability to have the courage to:

- Push back on unfair practices

- Leave toxic jobs without fearing for your mortgage

- Stay true to your values without worrying about next month’s bills

This is often the real reason why so many people want to retire early. It’s not about doing nothing, but to stop doing things they don’t believe in.

Build a Portfolio That Doesn’t Depend on You Watching the Market

To reach that kind of freedom, you do not need a fancy investment strategy. You need one that’s:

- Simple to execute

- Consistent over the long term

- Doesn’t require constant decisions or monitoring

That’s why many of our clients build portfolios using a combination of index ETFs and unit trusts, and combine it with a dollar-cost averaging system that runs automatically in the background.

Instead of trying to beat the market, you just need to capture a portion of its long-term returns consistently.

When you do this well, your investment portfolio becomes the second engine in your life, quietly compounding while your career continues to generate income.

Over time, the balance shifts. You become less reliant on your job. And that’s when freedom starts.

Why You Should Unbundle Your Insurance and Investments

One of the most common mistakes we see is people being sold bundled products like ILPs (Investment-Linked Policies) often early in their careers.

On paper, these look convenient: insurance and investments in one. But in reality, you lose:

- Transparency

- Flexibility

- And often, money

And you get the credit for supporting a friend.

But when you unbundle your insurance from your investments, you regain control.

Instead of choosing a bundled product:

- You can buy pure protection like term insurance for far less

- You can choose investments that suit your goals, timeline, and risk appetite

- You can compare prices and benefits more clearly in each category

And because insurers and investment platforms have to compete separately, this structure is usually cheaper and more efficient for you.

If I could paraphrase what Alex explained in the podcast:

“When the insurance company gives you back cash value, part of your premium went into coverage, and part went into savings. When you lump them together, it’s harder to compare. Unbundling gives you better cost transparency.”

A System That Supports the Life You Want

Whether your goal is early retirement, part-time work, or simply more freedom to say “no”, the building blocks are the same:

- Protect your income because it’s your biggest asset

- Invest simply and consistently to create a machine that builds your future income

- Unbundle insurance and investments to have more choice and better control

- Live below your means so you can focus on accumulating freedom, not just stuff

You don’t need to be a millionaire. You just need enough to create a buffer, so your values don’t get compromised by fear.

Final Thoughts

Alex didn’t retire early by chasing the highest return or living an extreme lifestyle. He did it by making intentional decisions:

- Controlling his spending

- Structuring his insurance and investments clearly

- And never forgetting that freedom is more valuable than luxury

If you’re a mid-career professional feeling stuck in the grind, his story is a reminder that you don’t need to win the game. You just need to stop playing someone else’s.

Want Help Building Your Own Freedom Plan?

If you’re ready to get intentional with your money, whether that’s simplifying your investments or reviewing your insurance, I’d love to help.

I work with mid-career professionals to create clear, flexible financial systems that align with your goals.

→ Book a free discovery call with me to have a conversation

Let’s build a system that supports the life you want.